Forget boomers vs millennials, the next conflict is millennials vs each other

Forget boomers vs millennials, the next conflict is millennials vs each other

[…] Demographically and electorally, boomers are now a fading force. And as the targets of millennial ire increasingly recede from view, they may soon be replaced by another privileged, property-owning elite much closer to home: millennials who have benefited from family wealth.

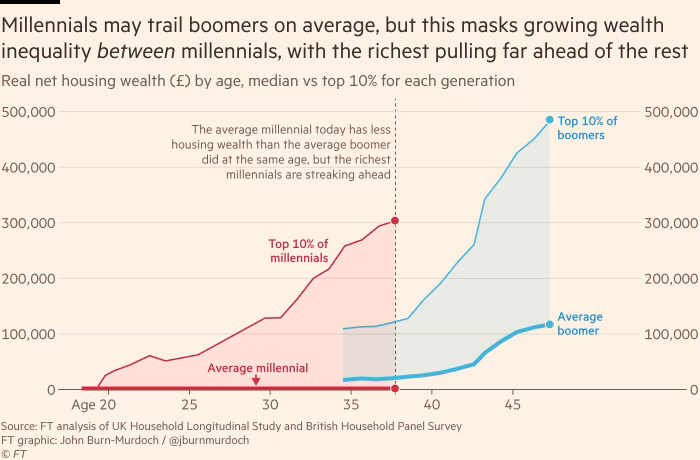

The millennials vs boomers discourse usually centres on the fact that, despite earning more than their parents’ generation, today’s young adults have been unable to translate that into home ownership and wealth more broadly. In the UK and US alike, the average millennial had accumulated less wealth in real terms by their mid-thirties than the average boomer at the same age. But this aggregate picture obscures what is happening at the top end of the distribution.

[…]

My analysis finds a similar picture in the UK. The average millennial still has zero housing wealth at a point where the average boomer had been building equity in their first home for several years. But the top 10 per cent of thirtysomethings have £300,000 of property wealth to their names, almost triple where the wealthiest boomers were at the same age.

So, while it’s true that in both countries the average young adult today is less well off than the average boomer was three decades ago, that deficit is dwarfed by the gap between rich and poor millennials, which is widening every year.

[…]

The fact that some thirtysomethings now own pricey homes in London, New York and San Francisco, despite it taking the average earner 20 to 30 years to save up the required deposit in these cities, gives away the open secret of millennial success: substantial parental assistance.

[…]

Bee Boileau and David Sturrock at the Institute for Fiscal Studies found that more than a third of young UK homeowners received help from family. Even among those getting assistance there are huge disparities, with the most fortunate 10th each receiving £170,000, compared with the average gift of £25,000.

And these gifts are not just one-off boosts; they compound over time. Say a British millennial in the top 10 per cent of gift recipients bought a home with a top 10 per cent price tag. Putting that gift towards their deposit would save them an additional £160,000 over a 25-year mortgage term due to the lower loan-to-value ratio afforded by a larger deposit and the resulting lower interest costs. This doubles the value of the gift received.

You're viewing a single thread.

This graph really shows how the focus on boomers by millennials and my fellow zoomers is really just a distraction from the real issues of class and wealth inequality.

Man, I've been beating that drum since the whole stupid "okay boomer" bullshit started.

Okay boomer isn’t about wealth inequality though?

It’s like saying incel is a distraction from class inequality, so we shouldn’t talk about them.

Boomerism is a mindset where you complain about the younger generation and think yours was great, it’s just named after the generation who put us all through the treatment.

No, it was and always has been about being a dick based on age. It, by nature, divides people by generation, and then age itself regardless of generation.

Anyone that thinks that every baby boomer is that kind of person is a bigger idiot than the boomers that do act, think, and speak like that.

A "generation" didn't put us through any treatment, any more than a "generation" is lazy, or out it touch, or anything.

The only real flaw of baby boomers as a generation is having the good luck to be born before assholes and sociopaths managed to tear apart the very structures that made the growth and wealth of the post war era possible.

Trying to claim that baby boomers were exclusively responsible for the southern strategy post Nixon, the eighties and the Reagan era policies that demolished real protection for the social net, and generally made things worse is plain dumb. The baby boomers weren't in fucking power until the tail end of that, and they were never a monolith any more than genX, millennials, or any generation after that.

Okay boomer as a thing is absolutely a distraction from a fundamental aspect of not just american economies and social mores (including wealth/class inequality), but the fact that all of that is a product of western society as a whole, going back to before the Americas were conquered and pillaged.

It's pure, blind, stupidity.