The "American Dream" costs far more than most people will earn over their lifetime

The "American Dream" costs far more than most people will earn over their lifetime

The cost of raising kids, buying a home and achieving other traditional milestones today far exceeds a typical worker's earnings, one analysis finds.

You're viewing a single thread.

Learn to invest and grow money ffs, don't just squander your income. At the bare minimum understand compound interest. The earlier the better

"Have you tried being richer?"

More like have you tried using your income more effectively?

They guy with an extra 10$ a month invested isn't in the same stadium as the guy with an extra 3k a month invested. 1 can retire, the other goes broke or in debt if they have car problems.

Okay grandpa. With what money? I only own a house due to inheritance.

Owning a house means no rent, most people blow 30% of their income on rent. Use that

The idea that workers can't understand compound interest, as though it's some crazy new idea, is a lie told by Capitalists to split the labor Aristocracy against the rest of the Proletariat.

Everyone knows that investing is good. Lying to engineers and doctors that they are somehow smarter and better than people who can't afford to invest just because engineers and doctors often can afford to invest is just a way for the bourgeoisie to protect itself from a United Proletariat.

What delusional nonsense are you dribbling? You've created some side argument for yourself nobody is talking about

You're blaming people's struggles with financial goals on poor planning and financial literacy, and making it a personal failure, rather than a systemic one. The reality is that people already understand basic financial literacy, but simply don't have enough income to meet basic financial goals regardless of budget.

Right until that next market crash. Dad was really happy in 2007.

You lose if you sell during a crash. If you bought literally just before the GFC and didn't sell, you would be up +313% on S&P 500. Buying at the worst time pre-GFC would have you negative for only 5 years.

Yeah I agree but if you planned to retire or planned to pay for a house or your kids college with that money you are SOL. Now you have to wait again on things that are time sensitive.

Yeah they said wait 5 years. If you're so desperate for cash u can't wait 5 years and work a part time job at 65 then fuck u just die.

I knew a guy where it did work out since he started school before the crash so they took the money out. Lucky him. Last crash cost me job so hurts worst when you need money and can't even sell stocks you were investing for times like this.

Can you give us a rundown on what you think is a good plan?

If we need to learn about compound interest. This is a good time to teach us.

Understand compound interest, how money grows over time. Learn to maximise your interest rate on savings and minimise interest rate on debts. If you have enough savings for an emergency fund, start investing excess savings into investment options that meet your personal risk threshold. Low risk options exist with high average yields (about 8%) like low fee ETFs tracking S&P 500 or other market indexes. My superannuation fund (retirement fund) has an average annual return of 12% for the past ten years, yields higher than this could impart higher than average risk of negative returns. Starting as early as you can lets you reap the benefits of compounding interest, snowballing income. Note that as interest rates go up, stock market returns usually decrease. If buying US stocks, make sure you DRS them otherwise you don't own them. I'm not a financial adviser, I'm just savvy with retail investing

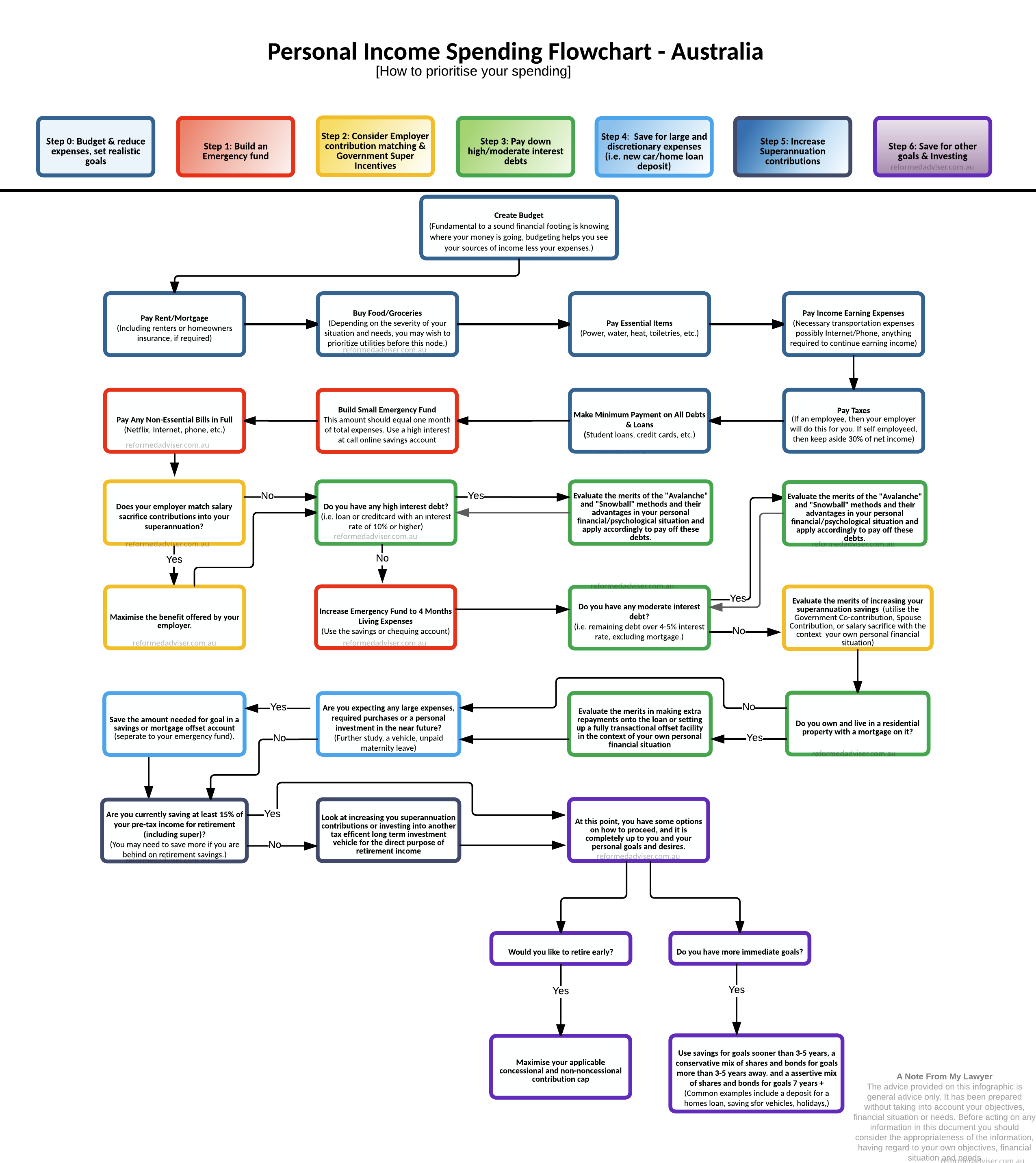

This flow chart is Australian but should loosely apply elsewhere too

Thats some nice info, but it doesn't explain what compound interest is.

When you get regular interest payments, that interest adds to the amount in the account so every interest payment your total interest paid increases. You can snowball this into a sizable figure with time, it pays more per year the longer you do it due to the snowballing. Especially if you find good interest rates and regularly review them

And where are these good interest rates and compounding services?

Essentially any account/financial product that pays interest into the account is compounding. Good interest rate accounts will vary on your country/area. Start by comparing savings account interest rates between your local banks and seeing if there are any special things you have to do to get the best rate. For example here with some banks they will pay an extra few % if you don't lower your savings account balance that month