Bulletins and News Discussion from April 1st to April 7th, 2024 - The Heydey of Juche - COTW: Democratic People's Republic of Korea

Bulletins and News Discussion from April 1st to April 7th, 2024 - The Heydey of Juche - COTW: Democratic People's Republic of Korea

Image is from this CNN article.

The DPRK's history has been a rollercoaster, with admirable highs and heartbreaking lows, most notably the Korean War and the fall of the USSR. Its steadfast commitment to Juche, a variant of Marxism-Leninism that focuses on self-sufficiency, has both made the DPRK a target for imperialist genocidal powers, and allowed them to survive these attacks.

Lately, we seem to be seeing a transition from surviving to thriving. China and the DPRK have always had a much more complicated history than Western education and media allows its population to know, with periods of quite strong disagreement - it's not the case that China is somehow the DPRK's master. Russia is the DPRK's other neighour that isn't US-occupied, and while they obviously differ substantially in ideology since the USSR fell, the tsunami of sanctions on Russia has changed things. The stick has been removed from the equation, with Russia facing no possible punishment from the West because they were unable to enact sanctions effectively and used all their ammunition in the first few barrages rather than turning the screws over time (I don't care if we're on the 14th sanctions package, it's all been meaningless for Russia since the end of 2022).

The carrot is also more visible, with an alliance making a lot of sense for both. Once again, Western education and media would have you believe a Parenti-esque reality in which Korea is a massive and unpredictable danger to the world, but is simultaneously so poor and destitute that their artillery pieces are made of wood and their missiles out of paper-mache. The truth is that Korea has innovated greatly in missile technology, with some of their weapons matching or even exceeding those of the Russians, hence the Russians' use of them in Ukraine. Russia also finds it advantageous to invest in Korea to strengthen the anti-hegemonic alliance's presence in the Pacific, countering the US-occupied lower half of the peninsula who has naturally sided with Ukraine. Additionally, Russia is investing deeply in the Arctic sea route. This will open up as climate change continues; is naturally quite defensible for Russia so long as Korea is there to provide further defense at its eastern edge; and is both a faster and safer route for Russia to access China - especially in a world where straits can be blockaded by even impoverished yet determined countries like Yemen. The situation in the Red Sea benefits Russia and China now, but in the coming years, the US may apply the same lesson for their own benefit elsewhere.

It is perhaps this new sense of self-confidence that has let Korea give up on reunification with its lower half via peaceful measures. A new Korean War would be devastating for both sides even if it remained non-nuclear, but with a rising DPRK and with the South falling yet further into hypercapitalist exploitation and misery, and a US that remains non-committal to its "allies" when times get difficult (as in Ukraine and Europe), a reality where Korea may finally hold the upper hand and have the ability to liberate its south may be approaching in the years and decades to come.

The COTW (Country of the Week) label is designed to spur discussion and debate about a specific country every week in order to help the community gain greater understanding of the domestic situation of often-understudied nations. If you've wanted to talk about the country or share your experiences, but have never found a relevant place to do so, now is your chance! However, don't worry - this is still a general news megathread where you can post about ongoing events from any country.

The Country of the Week is *the DPRK! Feel free to chime in with books, essays, longform articles, even stories and anecdotes or rants. More detail here.

Please check out the HexAtlas!

The bulletins site is here!

The RSS feed is here.

Last week's thread is here.

Israel-Palestine Conflict

Sources on the fighting in Palestine against Israel. In general, CW for footage of battles, explosions, dead people, and so on:

UNRWA daily-ish reports on Israel's destruction and siege of Gaza and the West Bank.

English-language Palestinian Marxist-Leninist twitter account. Alt here.

English-language twitter account that collates news (and has automated posting when the person running it goes to sleep).

Arab-language twitter account with videos and images of fighting.

English-language (with some Arab retweets) Twitter account based in Lebanon. - Telegram is @IbnRiad.

English-language Palestinian Twitter account which reports on news from the Resistance Axis. - Telegram is @EyesOnSouth.

English-language Twitter account in the same group as the previous two. - Telegram here.

English-language PalestineResist telegram channel.

More telegram channels here for those interested.

Various sources that are covering the Ukraine conflict are also covering the one in Palestine, like Rybar.

Russia-Ukraine Conflict

Examples of Ukrainian Nazis and fascists

Examples of racism/euro-centrism during the Russia-Ukraine conflict

Sources:

Defense Politics Asia's youtube channel and their map. Their youtube channel has substantially diminished in quality but the map is still useful.

Moon of Alabama, which tends to have interesting analysis. Avoid the comment section.

Understanding War and the Saker: reactionary sources that have occasional insights on the war.

Alexander Mercouris, who does daily videos on the conflict. While he is a reactionary and surrounds himself with likeminded people, his daily update videos are relatively brainworm-free and good if you don't want to follow Russian telegram channels to get news. He also co-hosts The Duran, which is more explicitly conservative, racist, sexist, transphobic, anti-communist, etc when guests are invited on, but is just about tolerable when it's just the two of them if you want a little more analysis.

On the ground: Patrick Lancaster, an independent and very good journalist reporting in the warzone on the separatists' side.

Unedited videos of Russian/Ukrainian press conferences and speeches.

Pro-Russian Telegram Channels:

Again, CW for anti-LGBT and racist, sexist, etc speech, as well as combat footage.

https://t.me/aleksandr_skif ~ DPR's former Defense Minister and Colonel in the DPR's forces. Russian language.

https://t.me/Slavyangrad ~ A few different pro-Russian people gather frequent content for this channel (~100 posts per day), some socialist, but all socially reactionary. If you can only tolerate using one Russian telegram channel, I would recommend this one.

https://t.me/s/levigodman ~ Does daily update posts.

https://t.me/patricklancasternewstoday ~ Patrick Lancaster's telegram channel.

https://t.me/gonzowarr ~ A big Russian commentator.

https://t.me/rybar ~ One of, if not the, biggest Russian telegram channels focussing on the war out there. Actually quite balanced, maybe even pessimistic about Russia. Produces interesting and useful maps.

https://t.me/epoddubny ~ Russian language.

https://t.me/boris_rozhin ~ Russian language.

https://t.me/mod_russia_en ~ Russian Ministry of Defense. Does daily, if rather bland updates on the number of Ukrainians killed, etc. The figures appear to be approximately accurate; if you want, reduce all numbers by 25% as a 'propaganda tax', if you don't believe them. Does not cover everything, for obvious reasons, and virtually never details Russian losses.

https://t.me/UkraineHumanRightsAbuses ~ Pro-Russian, documents abuses that Ukraine commits.

Pro-Ukraine Telegram Channels:

Almost every Western media outlet.

https://discord.gg/projectowl ~ Pro-Ukrainian OSINT Discord.

https://t.me/ice_inii ~ Alleged Ukrainian account with a rather cynical take on the entire thing.

You're viewing a single thread.

I don't have the time to summarize this at the moment, but this piece from 2021 linked in nakedcapitalism.com on "is the PRC more financialized than the US?" is interesting. I'm curious what our local China heads have to say about this (@Kaplya@hexbear.net ?)

Original piece: https://www.cogitations.co/p/financialization-is-it-worse-in-the

Nakedcapitalism commentary https://www.nakedcapitalism.com/2024/04/on-a-relative-scale-theres-a-strong-case-that-financialization-is-worse-in-the-prc-than-the-us.html

Apparently, Michael Hudson replied in the Nakedcapitalism comments:

I’m fine with this article. It says just what I’ve been saying in China.

Idid indeed say that China does not have the financialization and FIRE sector problem that the US and West has. It has its OWN FIRE sector problem. That’s what all my lectures in China are about.

One great difference is that China creates money and credit. It is able to write down debt with quite a different set of vested interests complaining.

There’s only one way to minimize the wealth inequality that these charts show. That’s to write down the debt. That will let some banks and companies and individuals go under. China can do that and survive.

At least it doesn’t have a systematic use of corporate debt to pay dividends, to buy stock to support its prices. It just debt-financed asset-price inflation — that is the common denominator. And it’s also China’s failure to tax land rent and other economic rent. That concept has not become mainstream, despite the fact that it was central to Marx (Vol. 3 esp.)

I’ve sent this article to my Chinese colleagues. I’ll let you all know what they say.

I wrote about this several times already, just not at this level of detail (and admittedly nowhere near the amount of research laid out in the article). Here’s one from last month.

It’s not so much like Wall Street financialization in the US, but the fact that there is simply way too much money thrown into real estate investment (including many companies that have nothing to do with real estate) that when the property bubble inevitably bursts (the government has to crack down the property market at some point, and has been doing so), a lot of their investments are going to evaporate.

It’s a very complex problem entangling the real estate developers, financial institutions and local governments - the three of them have been chained together in such a way that if one of them inevitably gets into trouble, they’re all screwed in one way or another.

The central government has to walk a tightrope in mediating the resolution of this issue. I don’t think damages can be avoided (though not to the level of the 2007 US subprime mortgage crisis), the question is how much can be mitigated? The system needs to be revamped if we’re being honest, the question is how to do this without adversely affecting the dozens and dozens of other sectors in the economy already linked to this?

I also talked about China going into deficit spending mode (i.e. turning to internal consumption mode to give money i.e. high wages to its own people to sustain a high level of domestic consumption) as a way to partially offset this imbalance. If people’s money (both households and corporations that have over-invested in real estate) are going to go up in smoke, the government HAS to spend much much more in order to keep the liquidity running in the economy.

In this case, turning China into a consumption economy is sort of inevitable (investment in China is already through the roof, more investment is not going to help, while the Western countries have been reducing their imports from China, so more exports isn’t going to help either. Consumption is the only way forward.) In other words, it’s time to make the Chinese citizens rich as a means of keeping the economy moving.

The difference between China and the US is that the latter is completely controlled by private banks, so when it comes to bailing out the economy, the people are the ones getting screwed (Obama let the bankers who stole $4 trillion to run free). China still has a state bank, so it has a lot more power to exert on the situation, but it’s not going to be easy.

Years ago I was able to chat with an economist at the Fed about the 2008/9 financial crisis (it was one of his areas of research). He wasn’t on the Board of Governors or anything he was a research economist, so he had a lot more freedom in exploring various explanations and paths of action.

In short, he basically said his research all pointed to the fact that the US should have followed what Sweden did in the early 90s and temporarily nationalize the banks. That would have saved the US a lot of pain - especially the pain homeowners felt. Bank shareholders ate the cat poop but homeowners were spared. Not perfect but way better than what Americans got - homeowners getting screwed and bank shareholders and bondholders bailed out.

All this to say, I think simply by not having a fully private banking sector (and having a DotP, of course), the real estate problem in China can be solved with relatively less pain. Having a centralized plan and ability to resolve makes a huge difference. It will be a tough pill to swallow, but it’s not insurmountable for China. The real estate crash in the US was bad but it was made worse by the political decision to only bail out capital and not homeowners. The US government chose to make the overall situation worse by maximally protecting the bourgeoisie, and taking no real steps to actually fix the underlying problems.

This could be an effort post on its own, but once again I have to raise the obvious Marxist objections to financialization. It is bad theory at best, extremely dangerous and straight up nonsense at worse.

First for some context, I already listed the very basics of the refutation some time ago here. The very short TL;DR is lots of people want an explanation, any explanation that exonerates the inherent problems with capitalism and for some Marxists that ignore Marx falling rate of profit. This is not about appealing just to Marx's authority but rather by ignoring these root causes and finding an "evil actor" i.e Wall Street you can propose some very charming solutions like regulations, taxes and even the usual vulgar terms like "industrial capitalism" as an opposite to "finance capitalism".

Ultimately the goal would be to rehabilitate capitalism with a promise that it can all change and it can all get better if only we remove the bad actors or we introduce these miraculous policies.

Skeptics might argue that if Sine is correct, why hasn’t the China-bashing media seized on his thesis? One possibility: depicting financialization, and in particular the level of US financialization, as bad is not something the Western business media is keen to promote. Even if the claims that China is cruising for a bruising include some financial metrics, like declining economic productivity of borrowing (how much incremental debt it now takes to generate a dollar more of GDP), debt levels, debt growth, real-estate related bankruptcies, the doubters tend to focus on the notion that China’s growth rate is flagging or overstated, and contend that that has knock-on effects, particularly making it difficult for China to deliver rising standards of living. They also point out the implications of China’s low birth rate.

For the mainstream, yeah? I wouldn't expect Business insider or WSJ to write about how Wall Street is bad actualy but do remember that the entirety of western mainstream critique of American capitalism is now captured by this rethoric and thanks to Bernie the solution is simple, just pay taxes, solve debt and give healthcare, everything will be solved.

But also this is superficial, as I mentioned in my other post, Biden wants to push this "industrialization" plan by bringing some high tech back to the US as if this will solve anything. This is the other facet of financialization, the belief that you can build factories in the US and that will solve American capitalism. This is an anti-Marxist fallacy. Not because factories are bad, no but rather American capitalist is already far too unprofitable and nothing short of a destruction of American living standards(wages) would allow these factories to be profitable now.

So while the MSM wont say "financialization bad" they'll say all the non-problematic things which supports the same conclusions.

The only way to keep a bigger financial system not to act as a drag is via strict regulation, something in absence these days.

Literaly showing the true colors! More regulation = problem solved, get rid of the bad actors and we can save capitalism!

Before going any longer, maybe its just me but most of these data points are 10 years out of date and maybe its just me but isn't this just bad form overall?

From here I can link to MR latest blog post on China. Yves wanted data? MR's post provides more than enough. China’s next decade

I'll compile Yve's quotes here than MR and you decide what actualy makes sense.

China has a savings rate of 50%, highest in the G-20, and mainly from households and non-financial companies. This lends some support to the complaint that China does not consume enough. Economic activity is sending more income and revenues to workers and their employers, but they aren’t plowing it back into the system by buying things, but by investing/speculating in real estate to an excessive degree. [This is their main point, and its bullshit as MR will show you]

Another sign of financialization is the rise in wealth disparity, with China approaching US levels” [If you read the charts carefuly, Chinese data stagnates between 2010-2014]

Remember, China does not have America’s student debt overhang or much use of credit cards and therefore presumably only pretty trivial credit card debt. But apps hand out microloans like candy and young borrowers reportedly fall prey to them. They do finance car purchases, but not as frequently as in the US.

But all the household dough is going overwhelmingly to real estate, with it accounting for 80% of typical net worth, versus 35% in the US. That much money going into property has unbalanced the entire economy:

Most of MR's post below with some of my emphasis. I'll summarize even further. Worrying about "consumer debt levels" or "the size of the banking sector" is pointless and mostly useless. It is mainstream economic theory realm which is just objectively incomplete and wrong on most areas.

When you talk about these things in the western context, its not that the finance sector is growing therefore things are bad. Rather "things are bad(profitability)" therefore the finance sector is growing.

MR's post

Despite this evidence, every year the Western ‘China’ experts (and even many in China itself) predict stagnation, given the huge debt levels in all sectors. China is going to stagnate like Japan has done in the last three decades. The only way to avoid ‘Japanification’, say these experts, is to ‘rebalance’ the economy from ‘over-investment’, ‘excessive savings’ and exports to a domestic consumer-led economy as in the West and reduce the state control of the economy so that the private sector can flourish.

This year on the occasion of the NPC, Martin Wolf, the Keynesian guru of the Financial Times, returned to this theme, echoing the arguments of other Keynesian China experts like Michael Pettis. According to Wolf, China’s growth will now slow to a trickle as in Japan because it overloaded with excessive debt and because it has not rebalanced the economy towards “the consumer”. China needs to get its consumption share up to Western levels or it will not be able to grow and so stay locked in a ‘middle income’ trap.

China generated 28 per cent of total global savings in 2023. This is only a little less than the 33 per cent share of the US and EU combined. This is all wrong, say Wolf and Pettis. What is needed is a shift from ‘excessive savings’ to consumption. There is over-investment in property and infrastructure, instead of handouts to households. China will only grow from here if consumption leads, not investment.

But how can anybody claim that the mature ‘consumer-led’ economies of the G7 have been successful in achieving steady and fast economic growth, or that real wages and consumption growth have been stronger there? Indeed, in the G7, consumption has failed to drive economic growth and wages have stagnated in real terms over the last ten years, while real wages in China have shot up. Moreover, these consumer-led economies have been hit by regular and recurring slumps in production that have lost trillions in output and income for their populations. The irony is that China’s consumption growth rate is way higher than in the G7 economies.

China has not had a contraction in national income in any year since 1976, while the consumer-led G7 economies have had slumps in 1980-2, 1991, 2001, 2008-9 and 2020. Much has been made of China’s ‘disastrous’ zero COVID policy. But apart from saving millions of lives, China still did not enter a slump in 2020, unlike all the G7 economies in 2020.

Yes, China has the highest ratio of gross investment to GDP among the major economies. But this supposedly ‘over-invested’, ‘excessive savings’ economy has grown more than four times faster than the consumer-led OECD economies and 40% faster than India as a result. What this suggests that if China were to ‘rebalance its economy towards the consumer and reduce investment; and reduce the public sector and ‘free up’ the private sector (the sector that provides most consumer goods in China), growth rates would fall even more than they have done in recent years.

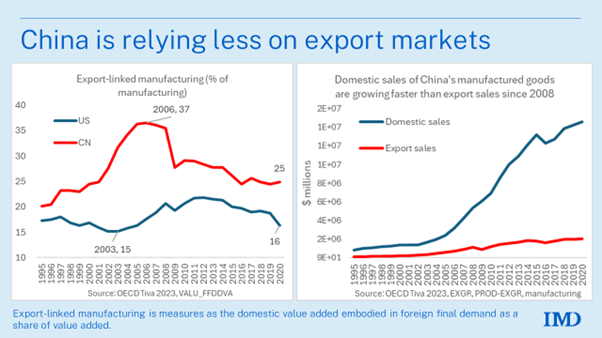

Moreover, the arguments of the Western experts that China is stuck in an old model of investment-led export manufacturing and needs to ‘rebalance’ towards a consumer-led domestic economy where the private sector has a free rein are just not empirically valid. Is China’s weak consumer sector forcing it to try and export manufacturing ‘over capacity’? Not according to a recent study by Richard Baldwin. He finds that the export-led model did operate up to 2006, but since then domestic sales have boomed, so that the exports to GDP ratio has actually fallen. “Chinese consumption of Chinese manufactured goods has grown faster than Chinese production for almost two decades. Far from being unable to absorb the production, Chinese domestic consumption of made-in-China goods has grown MUCH faster than the output of China’s manufacturing sector.”

What the Chinese government now needs to do is take over these large property developers and bring them back into public ownership, complete the projects and switch to building for rent. The government should annul the developers’ debt to foreign investors and only meet obligations to small investors; and end the mortgage and private finance system permanently. The unproductive real estate sector has got so large in China as a share of investment and output that it has seriously degraded growth. This is where the economy does need rebalancing. There needs to be a switch to productive investment in technology and knowledge industries. If the words of the Five-Year Plan mean anything, it seems that the current Chinese leadership is aware of that.

Once again, Roberts doesn’t know what he’s talking about, at least when it comes to China.

Yes, China’s consumption has gone up, so it doesn’t have a weak consumer base, right?

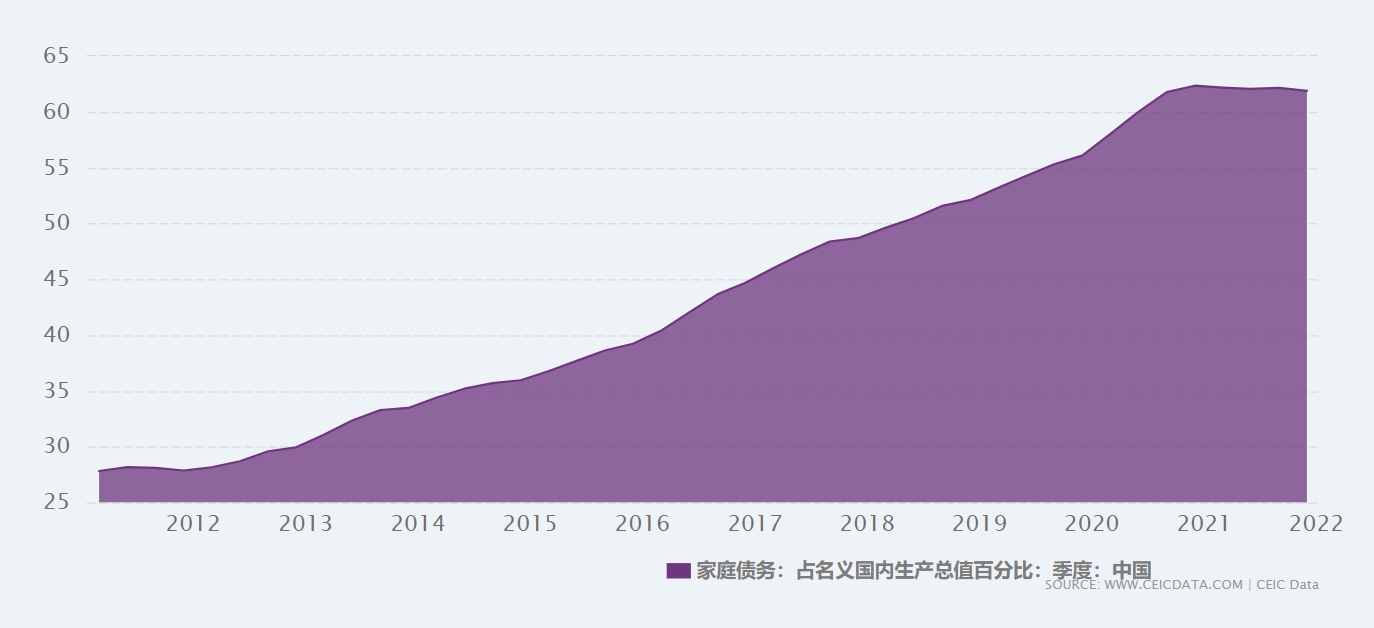

Except that both household and corporate debt have also gone up exponentially for the past decade:

Figure: Household debt to % of GDP, which more than doubled from <30% in 2011 to 62% in 2021People are borrowing to spend, and although this is still nowhere near as bad as in Western neoliberal countries, it’s not a good trend to persist. Going too far and your economy eventually becomes one that is fueled by credit, and that means if people stop borrowing to spend (because they can no longer repay their debt), then the economy is going into recessionary spiral. This is why writing down debt or cancelling them altogether is so important.

And ironically, China’s real estate problem today came precisely from the huge investment spending after the 2009 financial crisis. China spent 4 trillion RMB to stimulate its domestic economy that followed the global consumptive slump of 2009, and while it did its job in stabilizing the Chinese economy and prevented a recession that was occuring elsewhere in the world, that huge investment was also itself a problem. Why? Because while exports are down and domestic consumption continues to be weak, where do you think all the investment money ended up? In the real estate sector, precisely. When the real economy could no longer drive growth, the virtual takes over. Property market first emerged in China after 2008 and all the money went into that part of the economy because that’s where your asset value can go up.

Local governments found themselves unable to finance their own government because of the global financial crisis, so instead of investing into the real sector that was not growing, they raised cash instead by selling land and allowed the property market to proliferate - uncontrollably - to make up for the loss in GDP from the real economy. Then they used that money to repay their old debt to the financial institutions, and in turn taking out more new loans from the banks to sustain their local development activities.

As you can see, really, the only way out for China is to build a strong consumer base that is not fueled by debt, but through increase in real wages and net assets (and hopefully, not the housing assets that are bound to crash at some point).

Domestic consumption is not weak on any long term measure. The percentage of CN manufacturing dedicated to exports has declined/stagnated for 10 years.

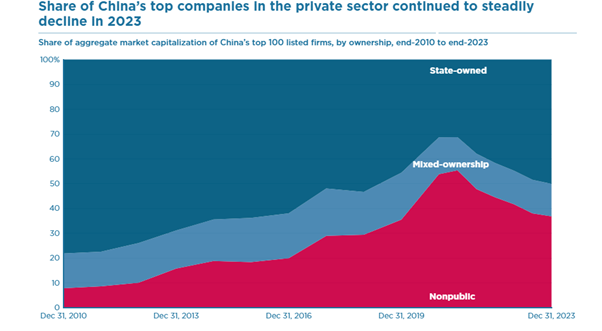

Not just that but also the share of the state sector is growing China versus the US

As you can see, really, the only way out for China is to build a strong consumer base that is not fueled by debt, but through increase in real wages and net assets (and hopefully, not the housing assets that are bound to crash at some point).

Ok lets be clearer. The Marxist approach is to increase the government control of the economy. For the capitalist side, the only thing that ought to matter is profitability. As long as the state controls key sectors we can also ensure capitalist exploitation doesn't increase.

China's success is based on this contradiction. The state must increase control while keeping exploitation in check yet capitalist profitability relies on constantly increasing exploitation? China gets to benefit from becoming the industrial center of the world, capitalist profitability can remain high(though it is dropping in CN now) as long as the government also covers all the social costs and keeps driving investment. More investment more production more consumption. Not the other way.

So far all the data supports this, China grows, state owned ownership grows DESPITE growing debt and growing unproductive sectors. For the economy to keep growing, only investment matters.

This is the central point. And what I said before at the very start, financialisation here got realy nothing to do with who is your favorite Marxist, but rather evil actor theory that NakedCapitalism and other right wing adjacent(and MSM with CN collapse fetish) would love to be true. If you can fix Capitalism you obviously don't need Communism.

IIPPE 2023 Part Two – China, profitability and financialisation

But Lo points out that industrial sector profitability remains high; it is the profitability of unproductive sectors like real estate and the stock market that has fallen back – and we know that China is facing a real estate crisis. Also, profitability has fallen because of a rising share of wages in value added (unlike in the West) and a rise in the organic composition of capital, following Marxist theory.

For me, Lo’s paper poses the major contradiction in China’s weird, hybrid economy. If the profitability of capital falls, that reduces investment and productivity growth in the capitalist sector. For me, that increases the need for China to expand its state sector to make the economy not so dependent on profitability, particularly in technology, education and housing.

In another session, Grzegorz Kwiatkowski and David Luebeck of the Berlin School of Economics looked at the degree of state control over companies in China. Of the 100 largest Chinese enterprises, there are 78 state-owned companies. The dominance of state-owned enterprises in the Chinese economy is much greater than in most other countries, reflecting the unique role they play in China’s economic system.

Again, this is something that I have outlined in my own work (see Capitalism in the 21st century p214). Using the IMF data on the size of the public sector for all countries, I found that, in 2017, China had a public investment to GDP ratio more than three times any other comparable economy, with the others averaging around 3% of GDP.

However the CPC did allow unproductive sectors aka financialisation, which is why there is only one correct way to handle it i.e taking ownership of the debt, erasing it while letting unprofitable/bankrupt business/investors go broke and pay their share. I think almost everyone agrees with this approach includinb both MR and Hudson.

For the Marxist perspective the solution is continue on the path of increasing government control, for the housing specificaly see below.

Surprise! The ‘over-invested’, ‘wildly unbalanced’ Chinese economy has delivered by far the faster consumption growth for its people – nearly four times faster than the consumer-led US, nine times faster than Japanification and even 50% faster than India. What this suggests that if China were to ‘rebalance’ its economy towards the consumer and reduce investment; and also reduce the public sector and ‘free up’ the private sector (the sector that provides most consumer goods in China), China’s growth rate would fall even more than it has done in recent years!

As it is, the consumption to GDP share graph is misleading. First, this measure of consumption excludes the social wage, particularly health and education, social care and public services. In countries like the US, much of this social consumption has to be paid for and so appears in the consumption share. That is not the case for much of social consumption in China. China has a long way to go in social consumption, but it is way ahead of its emerging market peers in many areas and not so far behind leading G7 economies, who started more than 100 years before.

Second, the graph shows consumption as a share of value-added (GDP) ie to the ‘final consumer’. In the US, consumption would seem to constitute 70% of GDP. However, if you look at ‘gross product’ which includes all the intermediate value-added products not counted in GDP, then consumption is only 36% of the total product; the rest constitutes demand from capital for parts, materials, intermediate goods and services. It is investment that is the swing factor and driver of demand, not consumption by workers.

What is true is that ‘productive’ investment growth has fallen back in China. Investment in new technology, manufacturing etc has given way to investment in unproductive assets, particularly real estate. In my view, successive Chinese governments made a big mistake in trying to meet the housing needs of its burgeoning urban population by creating a housing for sale market, with mortgages and private developers being left to deliver. Instead of local governments launching housing projects themselves to house people for rent, they sold state assets (land) to capitalist developers who proceeded to borrow heavily to build projects. Soon housing was no longer “for living but for speculation” (Xi quote). Private sector debt rocketed – just as in the real estate bubble in the West. It all came to a head in the COVID pandemic as developers and their investors went bust.

The real estate crisis has remained unresolved. It is interesting to see what the Western experts reckon is the solution. This is what Michael Pettis says: “Unfortunately, it will require a revival of speculative buying to prevent further contraction in the property sector and real estate prices, something which would only make things worse in the medium to long term.” (Tweet, 5 March). So the answer to the property crash is more speculation even if it makes things worse in the future!

That’s not my solution. What the Chinese government needs to do is take over these large developers and bring them back into public ownership, complete the projects and switch to building for rent. The government should end debt payments to foreign investors and only meet obligations to small investors; and transfer housing out of the mortgage and private finance system.

The real estate sector has got so large in China as a share of investment and output that it has seriously degraded overall growth. This is where the economy does need rebalancing. Outgoing PM Li said that China needed to “expand market access” for foreign investors, ‘prop up’ consumption and control risk in the real estate sector. Li pledged to help “high-quality, leading real estate enterprises” while continuing to “prevent unregulated expansion”.

Really, can Li square the circle? China’s private sector has mushroomed in the last two decades. It has led to an unhealthy expansion of billionaires and rising inequality of wealth and incomes. And just as in the West, as the profitability of productive capital fell, the capitalist sector switched into unproductive investment areas, like finance and real estate. Debt has rocketed. This has increased the risk of economic crises as in the West.

How do Chinese households borrow to consume if both their savings growth, their income growth and the consumption growth have been comfortably and sustainably larger than HH debt growth. HH debt can also be a bunch of things not related to most aspects of consumption so unless we have some ready to go data we cant know where that debt went and its a huge leap to call China's consumption growth "debt fueled". Like HH have to borrow to be able consume but also HH savings are at the same time growing faster and higher than HH debt ? They get in debt to be able to sustain their consumption but also they are able save up more than the debt they get into ? Doesnt pass the smell test.

Also the aggregated debt figure compared nominaly against the GDP may tell us absolutely nothing about how distressed the average household balance sheet is given the income and regional inequalities in China in the last decade and the economic activity of different groups. Its much more likely that upper middle housholds and individuals leveraged too much on the property market and speculation (irregardless of their returns) and on the average household level i would imagine most debt figures have accumulated from the explosion of car purchases and payments that foundementaly add a bunch to HH debt calculation no matter how healthy peoples balance sheet is. So Its less of an issue if HH debt going up mostly as a function of mortgage penetration for higher income earners but not coming at the expense of savings or consumption (but also not financing those things) for the average houshold.